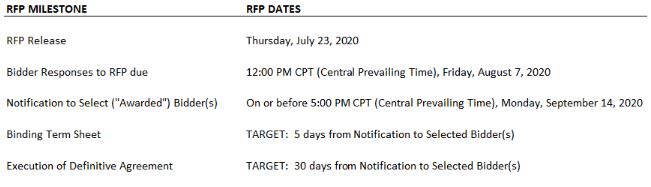

Northern Indiana Public Service Company ("NIPSCO") is soliciting a Request for Proposals for MISO capacity (Zonal Resource Credits "ZRC") covering MISO Planning Years 2021-2022, 2022-2023, and 2023-2024. Interested Bidders should refer to the attached RFP documents for the event details and requirements.

Event Summary:

RFP: Minimum 50 ZRC of MISO Capacity delivered to Local Resource Zone 6 for MISO Planning Years 2021-2022, 2022-2023, and 2023-24.

Please note the RFP minimum offer quantity is 50 ZRC.

It is also the responsibility of the Bidder to deliver the capacity to MISO Local Resource Zone 6 (if applicable, e.g. capacity is in a different Local Resource Zone or pseudo-tied into MISO).

Thank you very much for your interest in NIPSCO's RFP.

In this legal update regarding the implementation of FERC Order No. 872, Jason Johns, Jennifer Mersing and Jessica Bayles of Stoel Rives LLP break down the most significant changes made by the order and how they will serve to limit PURPA’s efficacy moving forward.

JASON JOHNS, JENNIFER MERSING, JESSICA BAYLES

The Federal Energy Regulatory Commission (FERC) issued Order No. 872 and implemented the largest overhaul to FERC’s regulations affecting Qualifying Facilities (QFs) in more than a decade. The order itself is 491 pages in length and there remain plenty of details to unpack in its implementation (including future proceedings to come at the FERC and state public utility commission level), but what is clear is that Order No. 872 substantially changes the ground rules for developing QFs.

Order No. 872 includes the following significant changes, among others: And while the order includes changes beyond the five listed below, the following are anticipated to have the most significant and immediate impact.

One-Mile Rule

Gone is the concrete presumption that projects located more than one mile from each other are considered to be at separate sites, for purposes of qualification as a QF. Now, only projects located 10 miles from each other will benefit from this presumption, while projects that are between one and ten miles from each other will only be afforded a rebuttable presumption. In addition to this change and for purposes of determining whether QFs are located at the “same site,” FERC will consider several new factors including, shared transformers or generation interconnection facilities, common debt and equity financing and common permitting and access rights.

None of these factors, which fall into the categories of physical characteristics or ownership/other characteristics, is dispositive in determining whether QFs are located at the “same site”; rather, FERC will weigh the evidence on a case-by-case basis.

Legally-Enforceable Obligations

A legally-enforceable obligation (LEO) represents that point in time when power purchase agreement pricing is locked in. Order No. 872 introduces new LEO regulations that require QFs to demonstrate commercial viability and a financial commitment to developing the project. FERC left it for each state to determine how a LEO is formed there, but it suggested that a QF be required to demonstrate that it has completed or undertaken site control for the project, filed an interconnection application and applied for the required permitting and zoning. Ultimately, FERC left it to each state agency to determine criteria for establishing a QF’s commercial viability and financial commitment.

Challenges to QF Status

Prior to Order No. 872, a party challenging the QF status of a project was required to seek a declaratory order from FERC, which carries a roughly $30,000 price tag. As the result of this order, parties challenging a QF’s status, including same site presumptions, need not pursue a declaratory order and therefore will avoid the associated fee. Substantive changes in the QF recertification include changes in electrical generating equipment that increase power production capacity by the greater of 1 MW, or 5% or a change in ownership, in which an owner increases its equity interest by at least 10%. Thus, a change in upstream ownership of an existing QF may open up that QF to challenges regarding aggregation with other affiliated same fuel source facilities within 10 miles.

Avoided-Cost Rates

Once again, FERC left it up to the states to come up with the proper method for determining a utility’s avoided costs. The order allows state agencies to eliminate fixed avoided-cost energy rates, while still retaining fixed capacity rates. Instead, the energy rates vary with changes in the utility’s as-available avoided costs as the energy is delivered. If the state decides to retain fixed energy rates, the fixed energy rate can now be based on project energy prices at the anticipated time of delivery.

There is a new rebuttable presumption that as-available energy rates can be based on locational marginal prices, if a utility is located within an organized market, or according to liquid trading hub prices or natural gas indices for those outside of organized markets. Avoided costs may also be determined through a competitive solicitation, provided it satisfies certain transparency and non-discriminatory procedures. States will now decide if QFs will bear merchant risk in their power sales arrangements.

Must-Purchase Opt Out

Lastly, for several years, utilities have been able to opt out of their obligation to purchase from QFs that are larger than 20 MW and located within an organized market. Yesterday’s order drops that threshold to 5 MW, meaning that utilities located within organized markets may apply to FERC for relief from the obligation to purchase power from QFs larger than 5 MW.

There is no avoiding the fact that Order No. 872 is a game-changer for QFs and utilities alike when it comes to PURPA, and yesterday’s order represents yet another instance where PURPA has become increasingly narrowed by FERC. There is more to play out with respect to Order No. 872 and we will provide further details as its implementation signals the order’s true scope.

Northern Indiana Public Service Company (NIPSCO) has announced its next two solar projects in the state, installations which, when completed, will nearly double Indiana’s entire installed solar capacity. The two projects were selected following a review of bids submitted through the all-source Request for Proposal (RFP) process that NIPSCO underwent late last year.

Brickyard Solar will be a 200 MW project developed, constructed, owned and operated by a subsidiary of NextEra Energy Resources. The installation will be located in Boone County and will include an estimated 675,000 solar panels. NIPSCO will purchase the power directly from Brickyard Solar through a 20-year purchase power agreement (PPA) when the project goes on-line some time in 2023.

The smaller of the set, Greensboro Solar will also be developed, constructed, owned and operated by a subsidiary of NextEra Energy Resources. Clocking in at 100 MW in capacity, along with 30 MW of battery storage, Greensboro will be located in Henry County and will include an estimated 329,500 solar panels. NIPSCO will purchase the power directly from Greensboro Solar through another, essentially identical 20-year PPA. Like Brickyard Solar, Greensboro is set to go online in 2023.

The 300 MW set to come to the Hoosier State via these two projects will nearly double the state’s total installed capacity thus far, which currently sits at 444 MW, good for 23rd most in the nation. Indiana is expected to add 1,357 MW of solar over the next five years.

These two projects don’t necessarily mean that NIPSCO is done procuring solar for 2020, as the utility shared that it expects to announce additional renewable projects later this year.

NIPSCO plans to be coal-free by 2028.

Please find below documents filed on 7/17/2020 by NIPSCO in Cause No. 45403:

There needs to be a Indiana statewide public spotlight on Vectren’s EDG tariff case before the IURC since it likely may set the pathway for the next four electric utilities—NIPSCO, Duke, IPL and I&M. to drastically reduce the amount paid to customers for excess DG. SEA 309 dictates that these DG tariffs must be filed no later than March 1, 2021.

Vectren’s new integrated resource plan puts increased reliance on large scale solar farm output but ignores customer owned solar facilities. Moreover, Vectren’s recent IURC filings seek to reduce the amount paid to Vectren customers for excess generation from their roof top solar units. This week the Indiana Utility Regulatory Commission (IURC) ruled against solar and net metering advocates with two rulings. First, over the objections of the Office of the Utility Consumer Counselor (OUCC), Indiana DG, Evansville solar installer Morton Solar and Solarize Indiana the Commission approved several 30-day filings from investor owned utilities requesting approval of annual avoided cost/PURPA rates . The objections suggested that these Vectren filings were not compliant with federal law under the Public Utilities Regulatory Policy Act (PURPA) requiring utilities to pay reasonable amounts for customer owned DG excess generation. Second the Commission denied a Motion to Consolidate the two Vectren 30-day filings with Vectren’s pending petition to establish Rider Excess Distributed Generation (EDG) in Cause No. 45378.

At stake is the establishment of fair and equitable rates for Vectren customers who produce their own power using solar panels, etc. The consumer groups contend that Vectren’s proposed Rider EDG must be compliant with federal law such as PURPA as well as Indiana law.

Vectren’s proposed EDG rate will not allow cost effective investments for customers with continued 1 to 1 credit of net excess using net metering vs. an anticipated excess DG rate of 3.1 cents.

The consequences of the requested adoption of Rider EDG is evident from what has transpired in other states such as Nevada. After effectively eliminating net metering in Nevada the rooftop solar market came to a grinding halt. The situation was finally remedied after a huge outcry from the public and action taken by the Nevada state legislature to reinstate net metering.

Across the state of Indiana, home owners, businesses, schools and local government interested in installing solar systems to achieve long term energy savings need to realize that although they are not Vectren customers, this case will likely establish an important precedence for the other four (4) investor owned electric utilities who may file similar petition’s with the IURC for low excess DG rates to replace net metering by March 1, 2021.

Thus far Indiana state legislators such as Rep. Ed Soliday (R-Valparaiso) who chairs the House Utility Committee and co-chairs the 21st Century Energy Task Force have not allowed for a comprehensive look at what is likely to happen to various businesses when net metering is eliminated. They have indicated that such a dialogue is still premature since technically net metering is not set to expire until 7/1/2022. Unfortunately, Vectren customers do not have luxury to wait. Vectren has indicated they want approval by the IURC for Rider EDG by the end of this year. Indications are also that NIPSCO will file for a DG tariff before the end of 2020.

Therefore, the time for action is now!

VECTREN WILL OFFICIALLY FILE ITS FINAL INTEGRATED RESOURCE PLAN (IRP) on 6/30/2020 WITH IURC

Although IndianaDG is pleased about some of Vectren’s preferred Portfolio, their IRP appears to ignore any meaningful contribution from Distributed Energy Resources (DERs) such as rooftop solar.

Vectren should design their next RFP expected this fall to provide better opportunities for smaller and more diverse solar resources. Vectren needs to modify the criteria to evaluate bids to give more favorable consideration to DERs.

We sincerely hope that the results from the Vectren Preferred Portfolio will not create another flurry of activities during the 2021 session of the Indiana General Assembly to throw a lifesaver to a sinking and uneconomic and dirty energy industry such as coal fired power plants.

Unfortunately, the state of Indiana appears to continue to lag behind in the high stakes competition with other states to bring new clean energy jobs and related economic development.

Will you contact your state legislators and candidates to explain action is needed now before it is too late?

Rooftop solar is worth 24¢/kWh in the Michigan territory served by Consumers Energy, well above the 14¢ to 17¢/kWh that the utility’s net metering customers currently receive for the electricity they send to the grid.

The Solar Energy Industries Association’s Director of Rate Design Kevin Lucas presented that finding in testimony in a Consumers Energy rate case.

Lucas concluded that rooftop solar “outflow energy” is “more valuable than average energy,” and that residential customers with solar are less costly to serve than other residential customers.

A key factor in the high value of rooftop solar, Lucas noted, is the “much lower” demand of customers with rooftop solar at the time of the system peak demand, compared to similar customers without solar. That means that customers with rooftop solar lower the system peak demand, thus reducing the need for costly generation and transmission capacity.

Rooftop solar customers, Lucas testified, also export much of their power during the utility’s “critical peak” hours of 2-6 p.m. on weekdays. He noted that the utility offers a “critical peak pricing” rate for residential customers designed to reduce afternoon demand on days when the utility calls a CPP event—when customers on that rate must pay 95¢/kWh for afternoon power.

Lucas proposed that Michigan regulators establish residential rates in a way that shares the savings created by rooftop solar, between those who own rooftop solar and other residential customers. He suggested that the savings be allocated 25% to rooftop solar owners, to incentivize further solar installations, and 75% to other residential customers, to drive residential rates down.

Lucas challenged a number of approaches used in a Brattle study that the utility used to show the cost of serving residential customers who have solar. He concluded that state regulators “should disregard the Brattle study upon which [the utility] relies.” Lucas describes his critique of the utility’s analysis, and presents his own analysis, in 68 pages of testimony.

Value of solar

Several organizations that jointly filed Lucas’s testimony, as well as testimony from other experts, recommended that Michigan regulators “initiate a comprehensive statewide study into the value of solar,” testified William Kenworthy, Vote Solar’s regulatory director for the Midwest.

Dr. Gabriel Chan, a University of Minnesota professor who testified in his personal capacity, suggested that Minnesota’s approach to a value of solar analysis could be a useful model.

The joint testimony was filed by the Environmental Law & Policy Center, on its own behalf and on behalf of the Ecology Center, the Great Lakes Renewable Energy Association, SEIA, and Vote Solar.